Financial literacy is often heralded as the cornerstone of financial success, with the assumption that understanding money management, budgeting, and investing will naturally lead to a stable and prosperous life. Yet, despite this knowledge, many financially literate individuals still find themselves grappling with money problems.

The question arises: Why do so many financially savvy people struggle with money? The answer lies in the complex interplay between knowledge and behavior, emotional decision-making, unforeseen life events, and the realities of an ever-changing economic landscape.

The Consumer Financial Survey revealed that about 70% of Americans do not have a detailed plan for managing their finances, and 44% do not keep a strict track of their spending. Approximately 41% of teens report not having received any financial knowledge for students or personal literacy education in school, indicating a significant gap in financial education that can carry into adulthood.

This lack of foundational knowledge can hinder effective financial decision-making later in life. This indicates that a significant portion of the population lacks the financial knowledge they believe they possess.

Have questions about this story?

Ask Tundra for more details, context, or updates.

Understanding The Facts And What Financial Literacy Typically Encompasses

Financial expertise refers to the ability to understand and effectively use various financial skills, including personal financial management, budgeting, investing, and understanding credit. It involves the knowledge and competencies needed to make informed and effective decisions regarding the use and management of money.

1- Budgeting:

Budgeting is the process of creating a plan to manage your income, expenses, and savings. It involves tracking your earnings, identifying essential and non-essential expenses, and allocating money to different categories to ensure that you live within your means. A well-crafted budget helps in prioritizing spending, avoiding debt, and setting aside funds for future needs or emergencies.

2- Saving and Investing:

Financial knowledge includes understanding the importance of saving money for short-term needs and long-term goals. This involves not only setting aside a portion of income regularly but also understanding different savings vehicles such as savings accounts, certificates of deposit (CDs), and money market accounts.

Investing goes beyond saving and involves allocating money to various assets, such as stocks, bonds, mutual funds, and real estate, with the goal of generating returns over time. It includes understanding the risks and rewards of different investment options, as well as strategies for building a diversified portfolio to meet specific financial goals.

3- Understanding Credit and Debt Management:

Credit literacy involves understanding how credit works, including how to build and maintain a good credit score, the implications of different types of credit (e.g. credit cards, loans), and how interest rates and fees impact the cost of borrowing.

Debt management is also a key component of finance literacy. This includes strategies for paying off debt efficiently, understanding the impact of debt on your overall financial health, and avoiding common pitfalls such as accumulating high-interest debt.

A survey by the National Foundation for Credit Counseling found that 65% of U.S. adults carry credit card debt from month to month, despite understanding the costs of interest. Emotions and social pressures can override financial knowledge.

4- Financial Planning:

Financial planning is the process of setting financial goals and developing a roadmap to achieve them. This can include retirement planning, saving for education, buying a home, and estate planning. Financial education encompasses understanding the tools and strategies available to create a comprehensive financial plan, such as retirement accounts (e.g. 401(k)s, IRAs), insurance, and tax-advantaged accounts.

5- Risk Management:

Understanding how to protect oneself against financial risks is another crucial aspect of financial information. This includes knowing how insurance works, the types of insurance available (e.g. health, life, disability, property), and how to choose the right policies to mitigate potential financial losses.

6- Tax Literacy:

It also involves understanding the basics of taxation, including how income is taxed, the importance of filing tax returns, and strategies for minimizing tax liability. This might include understanding deductions, credits, and tax-advantaged accounts that can help reduce taxable income.

7- Consumer Rights and Responsibilities:

Financial education includes being aware of consumer rights, understanding the terms and conditions of financial products and services, and knowing how to protect oneself from fraud and scams. It also involves being informed about the legal aspects of financial agreements, such as loan contracts and leases.

8- The Limitations of Financial Knowledge:

It is a powerful tool, equipping individuals with the knowledge needed to manage money effectively. However, possessing financial knowledge does not always translate into successful financial behavior.

Several factors contribute to the gap between what people know and how they act, revealing the limitations of financial knowledge.

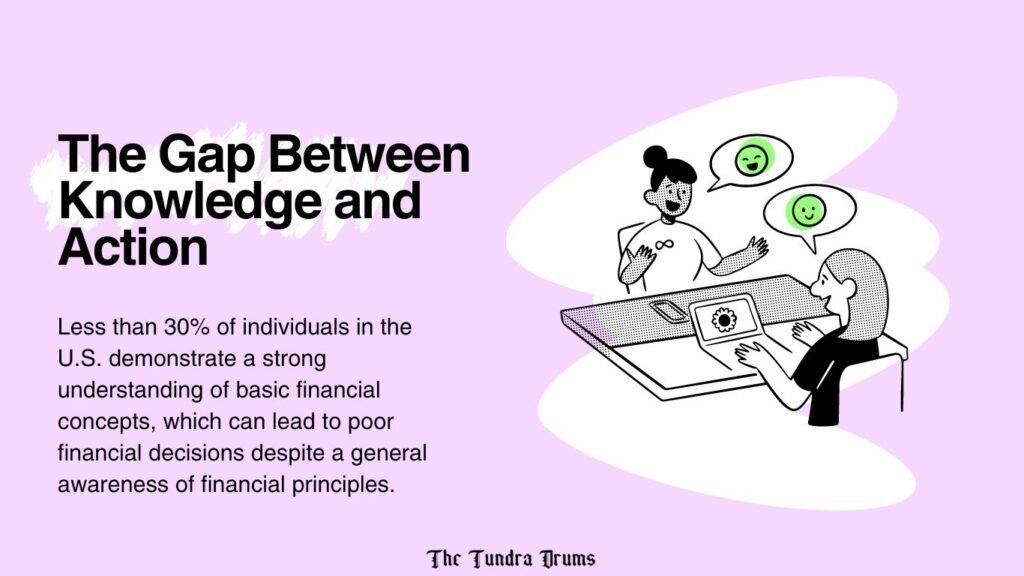

The Gap Between Knowledge and Action

Despite understanding key financial principles, many individuals struggle to apply this knowledge effectively in their daily lives. This gap between knowledge and action can be attributed to several factors:

- Procrastination and Lack of Discipline: Knowing the importance of saving or investing is one thing, but consistently setting aside money requires discipline and a commitment to long-term goals. Many people intend to save more or start investing but delay taking action, often due to competing short-term desires or simply a lack of habit. This procrastination can lead to missed opportunities and financial setbacks.

- Complexity and Overwhelm: The financial world is increasingly complex, with a wide array of products, services, and investment options. Even those with financial knowledge can feel overwhelmed by the choices and the need to stay updated on new developments. This complexity can lead to decision paralysis, where individuals avoid making decisions altogether for fear of making a mistake.

- Overconfidence and Misjudgment: Financially literate individuals may fall into the trap of overconfidence, believing that their knowledge will protect them from financial mistakes. This overconfidence can lead to taking on excessive risk, underestimating potential downsides, or failing to seek advice when needed. As a result, even well-informed individuals can make poor financial decisions.

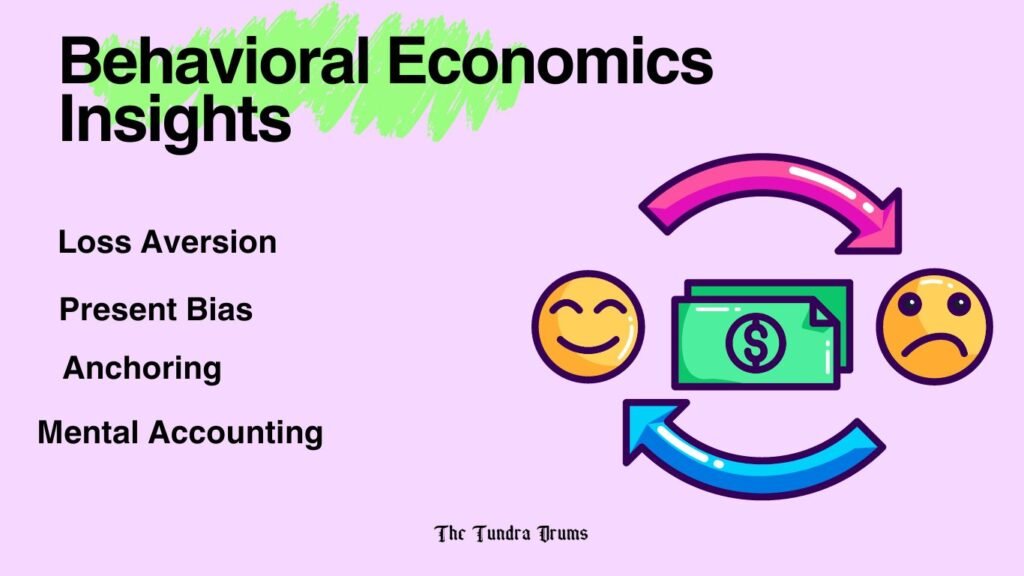

Behavioral Economics Insights

Behavioral economics provides valuable insights into why people often make poor financial decisions, even when they are financially literate. Some key concepts from this field include:

- Loss Aversion: Loss aversion is the tendency to prefer avoiding losses over acquiring equivalent gains. For example, the pain of losing $100 is generally more intense than the pleasure of gaining $100. This bias can lead to irrational financial decisions, such as holding onto losing investments too long or being overly cautious with money, even when opportunities for gain are present.

- Present Bias: Present bias refers to the tendency to prioritize immediate rewards over long-term benefits. Despite knowing the importance of saving for the future, many people struggle to delay gratification, opting for immediate spending instead. This can result in insufficient savings and a lack of preparedness for future financial needs.

- Anchoring: Anchoring occurs when individuals rely too heavily on the first piece of information they encounter (the “anchor”) when making decisions. For example, someone might base their investment choices on a single, memorable piece of advice or the initial price of a stock, rather than considering a broader range of information. This can lead to suboptimal financial decisions, as the anchor may not be relevant or accurate in the current context.

- Mental Accounting: Mental accounting is the tendency to categorize money into different “accounts” based on subjective criteria, such as the source of the money or its intended use. For instance, people might treat a tax refund as “extra” money to be spent on luxuries, even though it could be better used for savings or paying down debt. This compartmentalization can lead to inconsistent financial behavior and missed opportunities for optimizing resources.

Emotional and Psychological Barriers

Emotions and psychological factors can significantly impact financial decision-making, often overriding financial knowledge:

- Stress and Anxiety: Financial stress can lead to anxiety, which in turn can impair decision-making. Under stress, individuals may resort to short-term fixes, such as using credit to cover expenses, rather than making rational, long-term financial decisions. The emotional burden of financial stress can also lead to avoidance behaviors, where individuals delay dealing with financial issues because they feel overwhelmed.

- Fear and Risk Aversion: Fear, particularly the fear of losing money, can prevent individuals from taking necessary financial risks, such as investing in the stock market or starting a business. Even financially literate individuals may hold excessive amounts of cash or invest too conservatively due to a fear of loss, missing out on potential growth opportunities.

- Impulse and Instant Gratification: Impulsive behavior and the desire for instant gratification can undermine long-term financial planning. Despite knowing the importance of budgeting and saving, the temptation to make spontaneous purchases or indulge in lifestyle upgrades can lead to overspending and debt accumulation.

- Social Pressures and Comparison: Social pressures and the desire to keep up with peers can lead to financial decisions that are inconsistent with one’s knowledge or long-term goals. For instance, the pressure to maintain a certain lifestyle or make status-driven purchases can drive overspending, even when individuals know the financial consequences.

Final Thoughts

The myth of financial literacy reminds us that knowledge, while powerful, isn’t always the golden ticket to financial success. It’s like knowing the rules of a game but still needing to navigate the unpredictable twists and turns that life throws your way. Sure, understanding finances is important—it’s the foundation. But to truly thrive, we need more than just knowledge; we need to recognize our biases, make disciplined choices, and sometimes seek help when things get too complex. It’s about blending what we know with what we do and acknowledging that sometimes, success comes from adapting to circumstances that knowledge alone can’t foresee. So, as you continue your financial journey, remember that wisdom is in the application, not just the information.