Starting and growing a small business can be both an exciting and challenging journey. One of the most critical aspects that determine the success of any small business is access to funding. Whether you are launching a new venture or looking to expand an existing one, having the right financial resources is essential. This is where small business funding and loans come into play, serving as the lifeblood of your business operations.

Funding encompasses various financial solutions designed to support entrepreneurs in achieving their business goals. Understanding the options available can help you make informed decisions and secure the funds needed to drive your business forward. Funding is crucial for covering startup costs, managing cash flow, purchasing inventory, hiring staff, and even navigating unforeseen challenges.

Different Types of Funding and Loans Available

Small business owners have access to a variety of funding options, each with its own set of advantages and considerations. A significant 71% of small businesses utilize personal savings for startup costs, while 67% rely on credit cards.

Additionally, only 16% of businesses are funded through bank loans, highlighting the reliance on personal and alternative financing methods. Traditional loans from banks offer substantial capital with structured repayment terms, while SBA loans provide government-backed support with favorable conditions.

Microloans cater to those needing smaller amounts of capital, and crowdfunding allows businesses to raise funds from a large number of people, often in exchange for early product access or equity. Other options include grants, venture capital, and invoice financing, each designed to meet different business needs and situations.

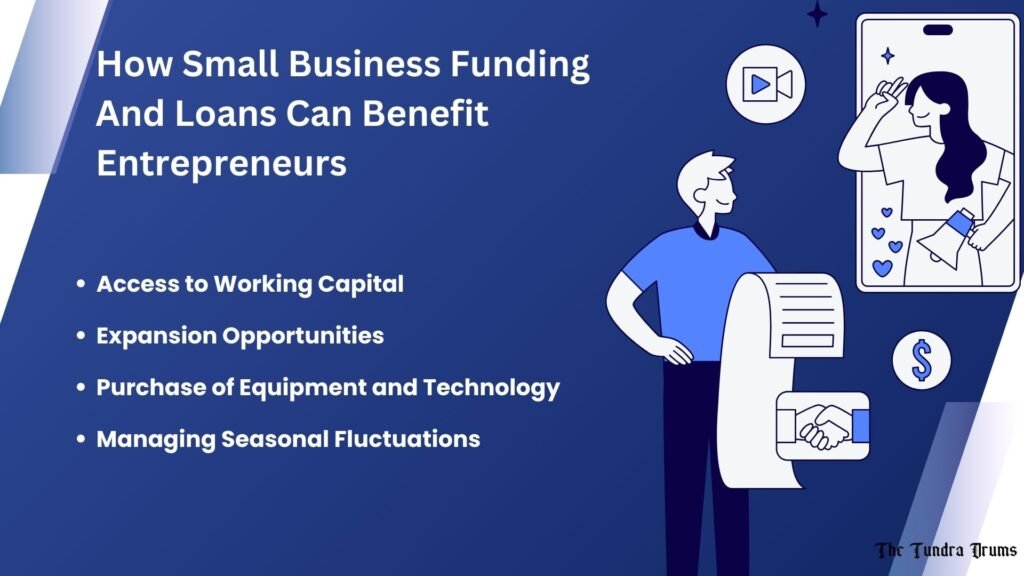

Effective Ways Small Business Funding And Loans Can Benefit Entrepreneurs

1. Access to Working Capital

Working capital refers to the funds that a business uses to manage its daily operations, including paying employees, purchasing inventory, and covering other short-term expenses. It is essentially the difference between a company’s current assets (like cash, accounts receivable, and inventory) and its current liabilities (such as accounts payable and short-term debt). Working capital is crucial because it ensures that a business has enough liquidity to meet its short-term obligations and continue its operations smoothly.

How Loans Provide Working Capital

Loans can be a vital source of working capital for small businesses, especially when there are temporary gaps between cash inflows and outflows. Short-term loans or lines of credit are commonly used to provide the necessary funds to maintain cash flow. These financial products allow businesses to cover immediate expenses while waiting for revenue from sales or other sources to come in.

Examples of Situations Where Working Capital is Crucial

Working capital is essential in various situations, such as:

- Inventory Purchases: Retailers often need to buy inventory in bulk ahead of peak seasons. Having access to working capital ensures they can stock up on products without straining their cash reserves.

- Payroll: A business must consistently pay its employees, even during slower sales periods. Working capital loans can cover payroll costs, ensuring that employees are paid on time.

- Unexpected Expenses: Businesses may face unforeseen expenses, such as equipment repairs or emergency maintenance. Working capital provides the flexibility to handle these costs without disrupting daily operations.

2. Expansion Opportunities

As a small business gains traction and begins to thrive, opportunities for growth and expansion often arise. These opportunities might include opening a new location to reach a broader customer base, increasing production capacity to meet higher demand, or launching new products and services. Expansion is a critical phase for any business, as it allows the company to scale operations, enhance market presence, and boost revenue. However, these growth initiatives typically require significant financial investment, which can be challenging for small businesses to fund out of pocket.

Using Loans for Expansion

Loans can play a pivotal role in supporting a business’s expansion plans. By securing the right funding, businesses can access the capital needed to turn growth opportunities into reality. For example, a loan can be used to:

- Purchase Property: Expanding to a new location often involves buying or leasing commercial property. A business loan can provide the necessary funds to acquire the right space without depleting the company’s cash reserves.

- Hire Staff: As a business grows, so does the need for additional staff. Loans can cover recruitment costs, salaries, and training expenses, ensuring the business has the human resources needed to support expansion.

- Marketing: To successfully expand, businesses often need to increase their marketing efforts to attract new customers and build brand awareness. A loan can fund marketing campaigns, advertising, and promotional activities that drive growth.

Case Study: Example of a Small Business That Expanded Using a Loan

Consider the example of “Bella’s Bakery,” a small, family-owned bakery that had been operating successfully in a single location for several years. With a growing customer base and increasing demand for their unique baked goods, the owners saw an opportunity to open a second location in a neighboring town. However, they lacked the necessary funds to purchase the new property, renovate the space, and hire additional staff.

Bella’s Bakery applied for a small business loan tailored for expansion. With the funds, they were able to secure the perfect location, make the necessary improvements, and bring on a team of skilled bakers and sales staff. The expansion was a success, leading to increased revenue and solidifying Bella’s Bakery’s reputation in the community.

This case illustrates how small businesses can leverage loans to seize expansion opportunities, enabling them to grow and reach new heights.

3. Purchase of Equipment and Technology

In today’s fast-paced business environment, modern equipment and technology are essential for maintaining competitiveness and improving operational efficiency. Whether it’s advanced machinery, state-of-the-art software, or specialized tools, investing in the right technology can significantly enhance productivity, reduce costs, and improve the quality of products or services. For small businesses, staying updated with the latest technology is crucial to meet customer expectations, streamline processes, and scale operations effectively.

Acquiring new equipment and technology often requires a substantial upfront investment, which can be a challenge for small businesses with limited cash flow. Fortunately, there are specific loans designed for equipment financing that provide the necessary funds to purchase or lease the equipment without straining the business’s finances. Equipment financing loans typically allow businesses to borrow up to the full cost of the equipment, spreading the payments over a fixed period. This approach enables businesses to upgrade their technology while managing cash flow effectively.

4. Managing Seasonal Fluctuations

Businesses that experience seasonal demand, such as those in retail, tourism, or agriculture, often face unique financial challenges. During peak seasons, these businesses may see a surge in sales, leading to increased revenue. However, during off-seasons, sales can drop significantly, causing cash flow issues. Managing these fluctuations is critical to the long-term success of seasonal businesses, as they must cover fixed expenses, maintain inventory, and retain staff even when sales are slow.

Loans to Smooth Cash Flow

To manage the financial ups and downs associated with seasonal fluctuations, many businesses turn to loans or lines of credit to smooth out cash flow. These financial products can provide the necessary funds to cover expenses during the off-season or to ramp up inventory and prepare for the busy season ahead. For example, a business might use a loan to purchase additional stock before the holiday rush or to cover payroll and other fixed costs during a slow period. By securing the right funding, seasonal businesses can maintain stability throughout the year, avoiding the strain of inconsistent cash flow.

Example of a Seasonal Business Utilizing Loans Effectively

Take the example of “Summer Breeze Surf Shop,” a small retail business located in a coastal town. The shop experiences a significant spike in sales during the summer months when tourists flock to the area but struggles to maintain cash flow during the off-season. To manage these fluctuations, the owner secured a line of credit that could be accessed as needed throughout the year.

During the winter months, the line of credit allowed Summer Breeze Surf Shop to cover rent, utilities, and payroll without dipping into reserves. As the summer approached, the shop used the funds to stock up on popular items, ensuring they were fully prepared for the tourist influx. This strategic use of loans allowed the business to remain operational and profitable year-round, despite the seasonal nature of its sales.

5. Improving Cash Flow

Maintaining healthy cash flow is critical for the survival and success of any small business. Cash flow refers to the movement of money in and out of a business, encompassing all the inflows from sales, investments, and other sources, as well as the outflows for expenses like payroll, rent, and inventory. Positive cash flow ensures that a business can meet its financial obligations, invest in growth opportunities, and handle unexpected expenses. Conversely, poor cash flow management can lead to difficulties in paying bills, and covering operational costs, and ultimately, can put the business at risk of insolvency.

Loans can serve as an effective tool for managing cash flow, particularly during periods when inflows are not sufficient to cover outflows. Short-term funding solutions, such as lines of credit or working capital loans, can provide immediate access to cash, helping businesses bridge temporary gaps in cash flow. For example, if a business is waiting on payments from clients but needs to pay suppliers or staff, a short-term loan can ensure that operations continue smoothly without interruption.

6. Building Business Credit

Building and maintaining a strong business credit profile is essential for small businesses seeking future funding opportunities. Business credit is similar to personal credit but applies to your business’s financial activities. A good business credit score demonstrates your company’s ability to manage debt responsibly, making it easier to qualify for loans, secure favorable interest rates, and negotiate better terms with suppliers. Moreover, strong business credit can provide a buffer during challenging times, as lenders are more likely to extend credit to businesses with a proven track record.

Using Small Loans to Build Credit

One effective way to build business credit is by taking out and responsibly managing small loans. By borrowing a manageable amount and making timely payments, a business can establish a positive credit history. Even a small loan can make a significant impact on your business credit score, as it demonstrates to lenders that your business can handle debt responsibly. Over time, as your business continues to meet its repayment obligations, your credit score will improve, opening up more substantial funding opportunities in the future.

Tips on Improving Business Credit Scores

- Separate Business and Personal Finances: Keep your business finances separate from personal accounts to establish a clear and professional credit history.

- Monitor Your Credit Report: Regularly review your business credit report to ensure that all information is accurate and up-to-date. Dispute any errors that could negatively impact your score.

- Pay Bills on Time: Consistently paying bills and loan installments on time is one of the most crucial factors in building a strong credit score.

- Limit Credit Utilization: Keep your credit utilization ratio low by not maxing out your credit lines. Using a smaller percentage of your available credit can positively affect your credit score.

- Build Relationships with Vendors: Establish accounts with suppliers and vendors that report to credit bureaus. Timely payments to these accounts will further enhance your credit profile.

7. Seizing Unexpected Opportunities

In the dynamic world of business, unexpected opportunities can arise at any moment, presenting both potential rewards and challenges. These opportunities might include acquiring a competitor, purchasing discounted inventory in bulk, entering a new market, or launching a new product. While these situations can offer significant growth potential, they often require immediate action and substantial capital. The challenge for small businesses is to act quickly and decisively, often needing funds that may not be readily available.

Leveraging Loans to Capitalize on Opportunities

Having access to quick funding through loans can make all the difference when it comes to seizing unexpected opportunities. A business that can secure a loan or line of credit promptly is better positioned to act on time-sensitive deals or strategic investments without having to deplete its cash reserves. For instance, if a business is presented with a chance to acquire a competitor at a favorable price, a loan can provide the necessary capital to close the deal quickly, potentially leading to substantial market share growth and increased revenue.

Real-World Example of a Business That Grew by Capitalizing on an Unexpected Opportunity

Consider the case of “Green Thumb Landscaping,” a small landscaping business that had been steadily growing its client base over several years. One day, the owner learned that a local competitor was looking to exit the business and was willing to sell their client contracts, equipment, and property at a discounted price. However, the owner needed to act quickly to secure the deal before another buyer stepped in.

Recognizing the opportunity to double the size of their business overnight, the owner applied for a short-term business loan. The loan was approved within days, providing the funds needed to acquire the competitor’s assets. As a result, Green Thumb Landscaping not only expanded its client base and service capacity but also established itself as a dominant player in the local market. This strategic move, made possible by quick access to funding, propelled the business to new heights.

8. Funding Marketing and Advertising Campaigns

Marketing and advertising play a crucial role in driving sales, building brand awareness, and ultimately contributing to the growth of any business. Effective marketing campaigns can help businesses reach new customers, strengthen relationships with existing ones, and differentiate themselves from competitors. Whether through digital marketing, social media, traditional advertising, or public relations, a well-executed marketing strategy can significantly boost a company’s visibility and revenue. However, successful marketing often requires a substantial investment, which can be challenging for small businesses with limited budgets.

Examples of Successful Marketing Campaigns Funded by Loans

One notable example is a small e-commerce business that sells handmade jewelry. The business had a loyal customer base but struggled to expand beyond its existing market. The owner decided to take out a small business loan to fund a comprehensive digital marketing campaign, including social media ads, search engine optimization (SEO), and influencer collaborations.

The loan allowed the business to create visually stunning ads, target specific demographics, and reach a much larger audience than before. Within a few months, the campaign significantly increased website traffic, leading to a substantial boost in sales and brand recognition. The return on investment from this marketing initiative was so strong that the business was able to repay the loan quickly while continuing to enjoy the benefits of increased brand visibility and customer engagement.

9. Hiring and Training Employees

Skilled and motivated employees are one of the most critical factors driving a business’s success. A talented workforce not only contributes to day-to-day operations but also plays a key role in innovation, customer service, and overall business growth. As a business expands, the need for additional staff and specialized skills becomes increasingly important. However, attracting, hiring, and training new employees can be costly, requiring significant investment in recruitment, onboarding, and ongoing professional development.

Case Study: Example of a Business That Grew by Investing in Its Workforce Through Loans

Consider the case of “Tech Innovators,” a small software development company that experienced rapid growth due to increasing demand for its services. However, the company struggled to keep up with the workload due to a shortage of skilled developers and project managers. To address this issue, the owner decided to apply for a business loan specifically to fund the recruitment and training of new employees.

With the loan, Tech Innovators was able to hire several experienced developers and project managers, offering them competitive salaries and comprehensive onboarding programs. Additionally, the company invested in ongoing training for its existing staff, focusing on the latest industry trends and technologies. As a result, the company not only expanded its workforce but also enhanced the overall skill set of its team

10. Emergency Situations and Contingency Planning

The world of business is inherently unpredictable, with potential emergencies that can arise at any time. These emergencies can take many forms, such as natural disasters like hurricanes, floods, or earthquakes that damage property and disrupt operations. Unexpected repairs, like a critical equipment breakdown, can halt production and lead to costly downtime. Additionally, economic downturns, supply chain disruptions, or public health crises, such as a pandemic, can significantly impact a business’s ability to operate smoothly. These situations can quickly escalate into major financial challenges, threatening the very survival of a business.

Example of a Business That Survived a Crisis Due to Timely Funding

One example of a business that survived a crisis thanks to timely funding is “Bright Horizons Daycare,” a small childcare center that served a local community. One winter, a severe ice storm caused extensive damage to the facility, including a collapsed roof and water damage to the interior. With the daycare forced to close for repairs, the owner faced the possibility of losing clients and revenue during the closure.

Fortunately, Bright Horizons had previously secured a line of credit as part of their emergency preparedness plan. The owner quickly accessed the funds to cover the cost of repairs, replace damaged equipment, and maintain essential expenses like staff salaries during the downtime. Thanks to the emergency funding, the daycare was able to reopen within a few weeks, minimizing the disruption to families and ensuring the business could continue serving the community.

The Bottom Line

Small business funding and loans offer numerous benefits, including providing essential working capital, enabling expansion opportunities, purchasing necessary equipment and technology, managing seasonal fluctuations, improving cash flow, building business credit, seizing unexpected opportunities, funding marketing campaigns, hiring and training employees, and serving as a safety net during emergencies.

These financial tools can significantly enhance a business’s ability to grow, compete, and navigate challenges. If you’re a small business owner, now is the time to consider how these funding options could benefit your specific situation. Take the next step by consulting with financial advisors or lenders to explore the loan options available and find the best fit for your business needs.